Stamp Duty Land Tax (SDLT) What are the basics?

Stamp Duty Land Tax (SDLT) What are the basics?

SDLT is paid to HM Revenue and Customs (HMRC) by the purchaser of a property in England. SDLT does not apply to property purchases in Wales. Buyers of Welsh properties will pay Land Transaction Tax to the Welsh Revenue Authority.

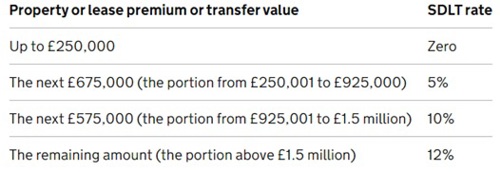

Following the mini budget in September 2022, the current basic rates of SDLT are as follows:

*********************************************************************************************************

First-Time Buyers’ Relief

If you are a first-time buyer, you can claim a discount (relief).

This means you’ll pay:

- no SDLT up to £425,000

- 5% SDLT on the portion from £425,001 to £625,000

You’re eligible if you and anyone else you’re buying with are first-time buyers. This means if you are buying jointly, you must both be first-time buyers to claim the relief.

If the price is over £625,000, you cannot claim the relief.

First-time buyers’ relief applies only in England. There's no first-time buyers’ relief in Wales.

Definitions:

First-time buyer: HMRC defines a first-time buyer as an individual or individuals who have never owned a major interest in a residential property in the United Kingdom or anywhere else in the world and who intends to occupy the property as their main residence.

Major Interest: HMRC defines a major interest in a dwelling as a freehold or leasehold interest originally granted for a term of more than seven years having a value of £40,000 or more at the date of the transaction.

*********************************************************************************************************

Additional Properties – Higher Rate SDLT

Higher rates of SDLT apply to purchases of additional dwellings.

Examples of transactions which attract the higher rates include:

- Purchase of second homes

- Purchase of buy-to-let properties

- Purchase of a new main residence where old main residence is still owned

- All dwellings purchased by companies

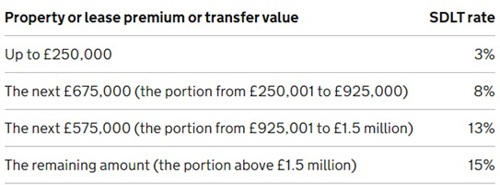

Following the mini budget in September 2022, the higher rates of SDLT are as follows:

If you sell or give away your previous main home within 3 years of buying your new home, you can apply for a refund of the higher SDLT rate part of your Stamp Duty bill.

You cannot get a refund if:

- you or your spouse still own any part of your previous home

- the higher rates still apply to you for another reason

Companies must pay the higher rates for any residential property they buy if the:

- property is £40,000 or more

- interest they buy is not subject to a lease which has more than 21 years left

If the property costs more than £500,000, the 15% higher threshold SDLT rate for corporate bodies may apply instead.

*********************************************************************************************************

Overseas/non-resident surcharge.

There is a 2% surcharge on residential properties in England and Northern Ireland bought by non-UK residents on or after 1 April 2021. The 2% surcharge applies on top of all other residential rates of SDLT including the higher rates for additional dwellings.

For the purposes of SDLT an individual is treated as UK resident if they have been in the UK for at least 183 days in any continuous period of 365 days falling within the two-year window beginning 364 days before the purchase and ending 365 days after it.

If the individual then subsequently satisfies the test to become UK resident, they can within two years of the purchase reclaim the surcharge. The refund is claimed by amending the SDLT return. This can be done within two years after the effective date of the transaction once the residence rule is satisfied.

Written by Hannah Oakes, Solicitor